⚡ Lighthouse Weekly

2026-06-05

This week's takeaway

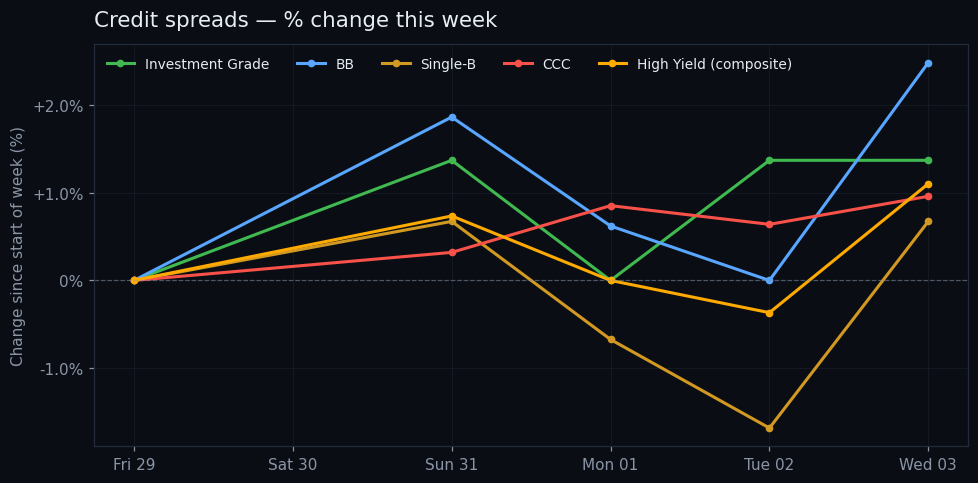

For the first time in weeks, every tier of the credit stack widened together. CCC is still leading (+0.12 on the week, +0.37 over 30 days to 9.47%, 76th percentile of the past 3 years), but BB, Single-B, and the HY composite all moved wider on both 1-day and 5-day windows. Absolute levels are still historically calm — HY composite at the 10th percentile, IG at the 1st — but the direction has flipped from 'CCC is the only tell' to broad-based drift. Composite stress score now 41.6, up from 36.9 two weeks ago.

📊 The state of play

The dispersion story has broadened. Two weeks ago only CCC was widening; this week BB sits at the 7th percentile (up from 4th), Single-B at the 30th (up from 25th), and every tier is red on the day. Absolute levels remain calm — markets are not panicking — but the direction of travel changed. The 2Y is up 0.13 over the past month and the 10Y-2Y curve flattened 0.08 percentage points over 30 days to 0.42, so the rates backdrop is doing some of the tightening work for the Fed without the Fed having to act.

📉 Credit stack

📰 The week in macro

- May payrolls came in at +172,000 with the unemployment rate unchanged at 4.3% (BLS Employment Situation), and ADP reported 122,000 private-sector adds — the biggest gain in 16 months — with broad-based sector strength (CNBC Economy). The labor data corroborates a still-resilient economy but not an overheating one.

- April job openings surged by 731,000 to 7.6 million, a near two-year high (CNBC Economy), reinforcing that labor demand is firming even as hiring freezes appear in pockets tied to rising input costs (MarketWatch).

- Treasury markets are showing fatigue ahead of the jobs print, with investors reportedly demanding more compensation to lend to the U.S. government (MarketWatch). Consistent with this, the 30Y sits at 4.99 and the 2Y rose 0.08 on the week to 4.08.

- A fresh redemption wave is hitting the $2 trillion private-credit market after two funds gated withdrawals in Q2 (MarketWatch). This sits alongside the CCC spread move (+0.37 over 30 days) as the clearest pocket of credit stress visible this week.

- Liquidity plumbing tightened: the Treasury General Account rose by $45.4 billion on the week to $875.7 billion, and bank reserves fell by $52.7 billion to $3.01 trillion (Fed H.4.1) — a quiet drain worth tracking.

📈 Rates

👀 Watching next week

Whether the dispersion accelerates or stalls.

BB and Single-B started widening this week but remain at calm absolute levels (7th and 30th percentile). The next step is whether they push meaningfully higher in the coming weeks. If yes, the regime has shifted. If no, this was a one-week wobble. CCC at the 76th percentile is the existing tell — watch whether it pulls the rest of the stack up with it.

Ready to ship?

✓ Looks good — send

Changes shown as: 1d = previous trading day · 5d = past trading week · 30d = past month.

Drafted by AI from Lighthouse data + scored news. Reviewed and edited by Graham before send.

Live dashboard: macrolighthouse.com

Drafted by AI from Lighthouse data + scored news. Reviewed and edited by Graham before send.

Live dashboard: macrolighthouse.com