⚡ Lighthouse Weekly

2026-05-29

This week's takeaway

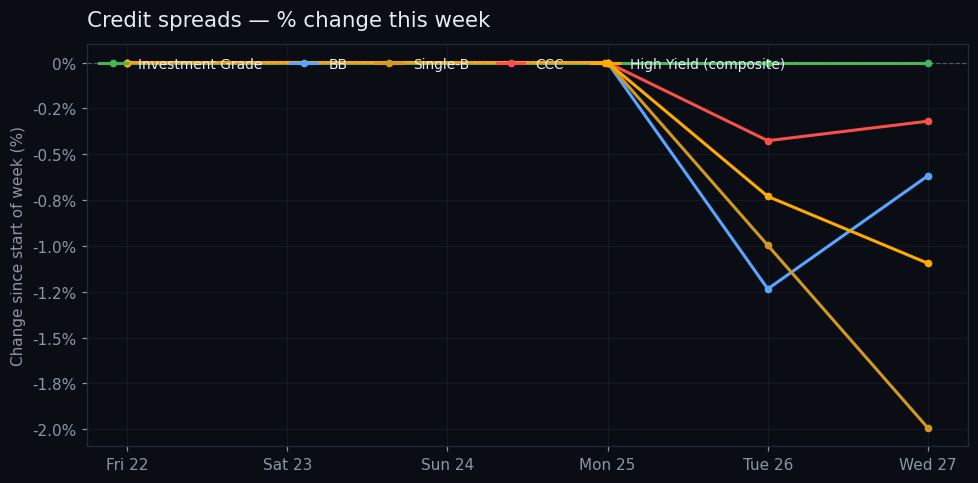

Credit spreads tightened across the stack this week even as Q1 GDP came in at a soft 1.6% and core PCE inflation (the Fed's preferred gauge) hit 3.3%. High yield composite spreads fell 9 basis points on the week to 2.71% — sitting in just the 6.8th percentile of the 3-year range — while the 10Y yield dropped 19 basis points to 4.48%. The market is paying for risk like conditions are benign, even as macro data says otherwise.

📊 The state of play

The composite reading is risk-on: HY at the 6.8th percentile and IG at the 0.5th percentile (effectively 3-year tights) suggest no credit stress is being priced, despite a curve that flattened 7 basis points (10Y-2Y now 0.46) and a 30-day rise in rates. CCC spreads remain the one tell — at 9.36% and the 70.5th percentile, up 28 basis points over 30 days — hinting that the weakest borrowers are not participating in the rally.

📉 Credit stack

📰 The week in macro

- Q1 GDP was revised to 1.6% — up from 0.5% in Q4 2025 (BEA) — a modest acceleration that still leaves growth running below the long-run trend, consistent with this week's spread tightening rather than widening (BEA News, MarketWatch).

- Core PCE came in at 3.3% year-over-year in April, the Fed's preferred gauge hitting a 3-year high, reinforcing the 'no cuts soon' stance from the new Warsh-led Fed (CNBC Economy, MarketWatch).

- Governor Waller's Frankfurt speech 'Policy Risks Have Changed' and MarketWatch reporting frame the regime as a hold — neither cuts nor hikes imminent — which helps explain why 2Y yields fell 13 basis points on the week even as rates remain higher over the past month (Federal Reserve Speeches, MarketWatch).

- The ECB flagged elevated financial stability vulnerabilities amid a 'geoeconomic shock' (ECB), while Bank of France's Villeroy told CNBC the ECB 'will do what is necessary' on inflation — with markets overwhelmingly pricing a rate hike at the next meeting. The Fed-ECB policy divergence is worth tracking against the dollar.

- CNBC reports family offices are trimming U.S. exposure in a 'de-dollarization' trade citing tariffs, debt and AI-bubble concerns — a flow story that bears watching against the 30Y at 5.01% (CNBC Finance).

📈 Rates

👀 Watching next week

Watch whether CCC spreads keep diverging from the broader HY rally.

CCC is up 28 basis points over 30 days and sits at the 70.5th percentile while BB (2.7th percentile) and the HY composite (6.8th percentile) are near multi-year tights — a classic late-cycle dispersion signal.

Ready to ship?

✓ Looks good — send

Changes shown as: 1d = previous trading day · 5d = past trading week · 30d = past month.

Drafted by AI from Lighthouse data + scored news. Reviewed and edited by Graham before send.

Live dashboard: macrolighthouse.com

Drafted by AI from Lighthouse data + scored news. Reviewed and edited by Graham before send.

Live dashboard: macrolighthouse.com